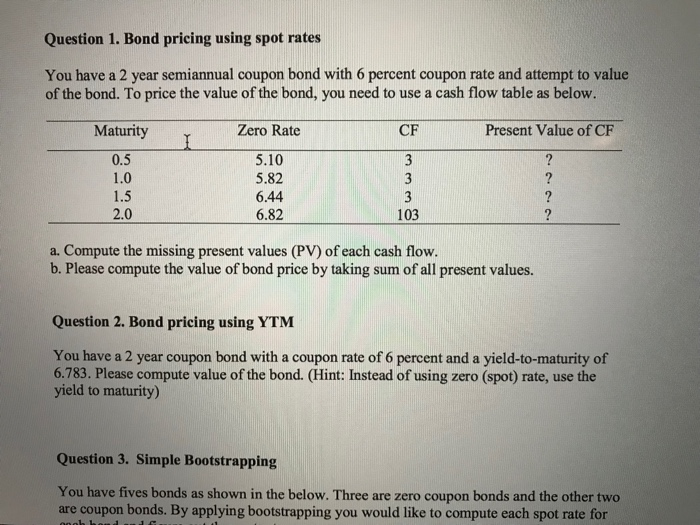

Question 1. Bond pricing using spot rates You have a 2 year semiannual coupon bond with 6 percent coupon rate and attempt to value of the bond. To price the value of the bond, you need to use a cash flow table as below. Maturity Zero Rate CF Present Value of CF 0.5 1.0 1.5 2.0 5.10 5.82 6.44 6.82 103 a. Compute the missing present values (PV) of each cash flow. b. Please compute the value of bond price by taking sum of all present values. Question 2. Bond pricing using YTM You have a 2 year coupon bond with a coupon rate of 6 percent and a yield-to-maturity of 6.783. Please compute value of the bond. (Hint: Instead of using zero (spot) rate, use the yield to maturity) Question 3. Simple Bootstrapping You have fives bonds as shown in the below. Three are zero coupon bonds and the other two are coupon bonds. By applying bootstrapping you would like to compute each spot rate for Question 3. Simple Bootstrapping You have fives bonds as shown in the below. Three are zero coupon bonds and the other two are coupon bonds. By applying bootstrapping you would like to compute each spot rate for each bond and figure out the spot rate curve. Bond MaturityCoupon Bond Price Zero Rates Principal 100 100 100 100 100 0.25 0.50 1.00 1.50 2.00 0 97.5 94.9 90.0 96.0 101.6 4 12 a. Compute the spot rate using the bootstrapping method. b. Draw the spot rate curve. c. Is that an upward slope or downward slope? d. What is the spread between a 2 year bond rate and a 6month yield? e. Based on the answer of d, do you think the slope is steep? Question 4. Compute forward fates You have a 10 year treasury bond with 5 percent coupon rate using spot rates. Maturity Zero Rate Zero Rate Forward Rate Semiannual Semiannual Discount PV of CF Factor Cash Flow 4.8077 5 0.9219 4.6095 5 0.8772 4.3859 5 0.8346 4.1730 5 0.7935 3.9676 0.5 0.08000 1.0 0.08300 1.5 0.08930 2.0 0.0924 2.5 0.0946 3.0 0.09787 3.5 0.10129 4.0 0.10592 4.5 0.10850 5.0 0.11021 5.5 0.11175 6.0 0.11584 6.5 0.11744 7.0 0.11991 7.5 0.12405 8.0 0.12278 8.5 0.12546 9.0 0.13152 9.5 0.13377 10.0 0.13623 0.0400 0.0415 0.0447 0.0462 0.0473 0.0489 0.04000 0.04300 0.05098 0.9615 0.05177 0.06096 0.06463 0.0506 0.0s69s 0.0530 0.0543 0.0551 0.0559 0.06283 0.0579 0.0587 0.0600 0.0620 0.0614 0.0627 0.0658 0.0669 0.0681 0.7508 5 0.7076 3.5382 5 0.6618 3.3088 5 0.6216 0.06361 0.08068 5 0.5848 2.9242 0.5499 2.7494 5 0.5088 2.5441 0.4763 0.4426 0.4055 0.3855 0.3555 5 0.3178 0.2923 2.3813 105 0.2677 28.1079 a Compute the missing forward rates in the table b. Compute the missing present values of cash flow. c. Compute the value of the bond Yuwen's - Question 6. You observe the Treasury yield curve below (all yild are shown on a bond equivalent basis) Yieldto Maturity 1000% Ycar 0.5 1.0 1.5 2.0 Spot Rate Forward Rate- 10.00% 9.75 9.50 9.25 9.75 9.48 9.22 9.00 8.50 8.00 8.95 8.68 8.41 8.14 7.86 7.58 7.30 7.02 6.74 6.46 6.18 5.90 5.62 5.35 3.0 3.5 4.0 5.0 5.5 7.50 7.25 7.00 6.75 7.0 7.5 8.5 9,0 9.5 10.0 6.25 6.00 5.75 5.50 05.25 All the securities maturing from 1.5 years on are selling at par. The 0.5 year and one-year securities are zero-coupon instruments. a. Calculate the missing spot rates b. Calculate the missing forward rates c. What should the price of the four year Treasuring security be

Answer & Explanation

Solved by verified expert

Get Answers to Unlimited Questions

Join us to gain access to millions of questions and expert answers. Enjoy exclusive benefits tailored just for you!

Membership Benefits:

Unlimited Question Access with detailed Answers

Zin AI - 3 Million Words

10 Dall-E 3 Images

20 Plot Generations

Conversation with Dialogue Memory

No Ads, Ever!

Access to Our Best AI Platform: Zin AI - Your personal assistant for all your inquiries!