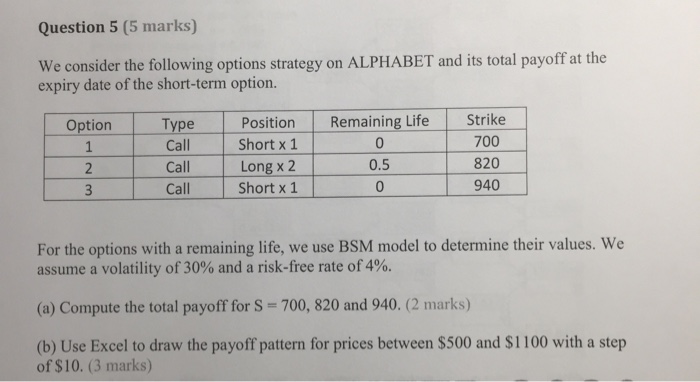

We consider the following options strategy on ALPHABET and its total payoff at the expiry...

60.1K

Verified Solution

Question

Finance

We consider the following options strategy on ALPHABET and its total payoff at the expiry date of the short-term option. Option | Type | Postion | Remaining Life | Strike 1 Call Short x 1 0 700 2 Call Long x 2 0.5 820 3 Call Short x 1 0 940 For the options with a remaining life, we use Black-Scholes-Merton (BSM) model to determine their values. We assume a volatility of 30% and a risk-free rate of 4%. a) Compute the total payoff for S = 700, 820, and 940 (2 marks) b) Use Excel to draw the payoff pattern for prices between $500 and $1100 with a step of $10. (3 marks)  Question 5 (5 marks) We consider the following options strategy on ALPHABET and its total payoff at the expiry date of the short-term option. Option Remaining Life Type Call Call Call Position Short x1 Long x 2 Short x 1 Strike 700 820 940 .5 0 0 For the options with a remaining life, we use BSM model to determine their values. We assume a volatility of 30% and a risk-free rate of 4%. (a) Compute the total payoff for S = 700, 820 and 940. (2 marks) (b) Use Excel to draw the payoff pattern for prices between $500 and $1100 with a step of $10. (3 marks) Question 5 (5 marks) We consider the following options strategy on ALPHABET and its total payoff at the expiry date of the short-term option. Option Remaining Life Type Call Call Call Position Short x1 Long x 2 Short x 1 Strike 700 820 940 .5 0 0 For the options with a remaining life, we use BSM model to determine their values. We assume a volatility of 30% and a risk-free rate of 4%. (a) Compute the total payoff for S = 700, 820 and 940. (2 marks) (b) Use Excel to draw the payoff pattern for prices between $500 and $1100 with a step of $10

Question 5 (5 marks) We consider the following options strategy on ALPHABET and its total payoff at the expiry date of the short-term option. Option Remaining Life Type Call Call Call Position Short x1 Long x 2 Short x 1 Strike 700 820 940 .5 0 0 For the options with a remaining life, we use BSM model to determine their values. We assume a volatility of 30% and a risk-free rate of 4%. (a) Compute the total payoff for S = 700, 820 and 940. (2 marks) (b) Use Excel to draw the payoff pattern for prices between $500 and $1100 with a step of $10. (3 marks) Question 5 (5 marks) We consider the following options strategy on ALPHABET and its total payoff at the expiry date of the short-term option. Option Remaining Life Type Call Call Call Position Short x1 Long x 2 Short x 1 Strike 700 820 940 .5 0 0 For the options with a remaining life, we use BSM model to determine their values. We assume a volatility of 30% and a risk-free rate of 4%. (a) Compute the total payoff for S = 700, 820 and 940. (2 marks) (b) Use Excel to draw the payoff pattern for prices between $500 and $1100 with a step of $10

Option | Type | Postion | Remaining Life | Strike

1 Call Short x 1 0 700

2 Call Long x 2 0.5 820

3 Call Short x 1 0 940

For the options with a remaining life, we use Black-Scholes-Merton (BSM) model to determine their values. We assume a volatility of 30% and a risk-free rate of 4%.

a) Compute the total payoff for S = 700, 820, and 940 (2 marks)

b) Use Excel to draw the payoff pattern for prices between $500 and $1100 with a step of $10. (3 marks)

Get Answers to Unlimited Questions

Join us to gain access to millions of questions and expert answers. Enjoy exclusive benefits tailored just for you!

Membership Benefits:

- Unlimited Question Access with detailed Answers

- Zin AI - 3 Million Words

- 10 Dall-E 3 Images

- 20 Plot Generations

- Conversation with Dialogue Memory

- No Ads, Ever!

- Access to Our Best AI Platform: Flex AI - Your personal assistant for all your inquiries!

Other questions asked by students

StudyZin's Question Purchase

1 Answer

$0.99

(Save $1 )

One time Pay

- No Ads

- Answer to 1 Question

- Get free Zin AI - 50 Thousand Words per Month

Best

Unlimited

$4.99*

(Save $5 )

Billed Monthly

- No Ads

- Answers to Unlimited Questions

- Get free Zin AI - 3 Million Words per Month

*First month only

Free

$0

- Get this answer for free!

- Sign up now to unlock the answer instantly

You can see the logs in the Dashboard.