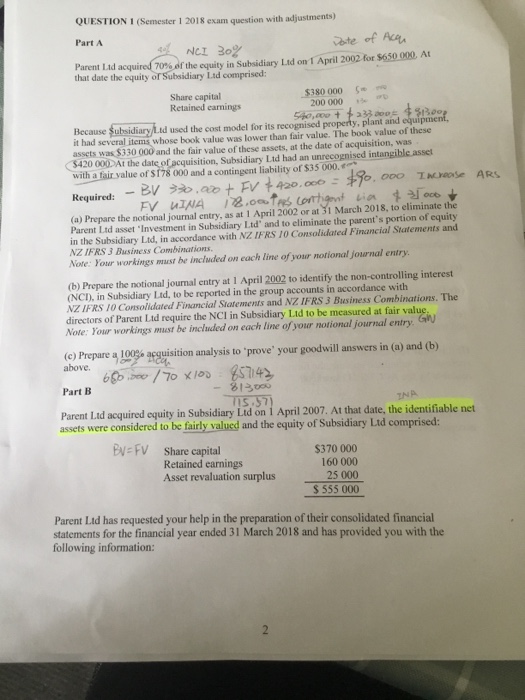

QUESTION 1 (Semester 1 2018 exam question with adjustments) Part A NCL 30 Parear Lad acquired 70ss of the equity in Subsidiary Ltd on 1 April 2002 for $650 00 At that date the equity of Subsidiary Ltd comprised: Share capital Retained earnings $380 000 200000 Because subsidiaryLud used the cost model for is recogmised property, plant and equipmnt it had several items whose book value was lower than fair value. The book value of these assets was $330 000 and the fair value of these assets, at the date of acquisition, was S420 000 Af the date of acquisition, Subsidiary Ltd had an unrecognised intangible asset with a fair value of $178 000 and a contingent liability of $35 000. Required:BV.ao t Fv t42o.oco:.ooo Zhoose ARs (a) Prepare the notional journal entry, as at 1 April 2002 or at 31 March 2018, to eliminate the Parent Ltd asset 'Investment in Subsidiary Ltd' and to eliminate the parent's portion of equity in the Subsidiary Ltd, in accordance with NZ IFRS 10 Consolidated Financial Statements and NZ IFRS3 Business Combinations Note: Your workings must be included on each line of your notional journal entry (b) Prepare the notional journal entry at 1 April 2002 to identify the non-controlling interest NZ IFRS 10 Consolidated Financial Statements and NZ IFRS 3 Business Combinations. The (NCI), in Subsidiary Ltd, to be reported in the group accounts in accordance with directors of Parent Ltd require the NCI in Subsidiary Ltd to be measured at fair value, Note: Your workings must be included on each line of your notional journal entry. G (e) Prepare a 100 acquisition analysis to 'prove' your goodwill answers in (a) and (b) Part B Parent Lid acquired equity in Subsidiary Ltd on i April 2007. At that date, the identifiable net assets were considered to be fairly valued and the equity of Subsidiary Lid comprised: EN-F Share capital $370 000 160 000 25 000 S 555 000 Retained earnings Asset revaluation surplus Parent Ltd has requested your help in the preparation of their consolidated financial statements for the financial year ended 31 March 2018 and has provided you with the following information: QUESTION 1 (Semester 1 2018 exam question with adjustments) Part A NCL 30 Parear Lad acquired 70ss of the equity in Subsidiary Ltd on 1 April 2002 for $650 00 At that date the equity of Subsidiary Ltd comprised: Share capital Retained earnings $380 000 200000 Because subsidiaryLud used the cost model for is recogmised property, plant and equipmnt it had several items whose book value was lower than fair value. The book value of these assets was $330 000 and the fair value of these assets, at the date of acquisition, was S420 000 Af the date of acquisition, Subsidiary Ltd had an unrecognised intangible asset with a fair value of $178 000 and a contingent liability of $35 000. Required:BV.ao t Fv t42o.oco:.ooo Zhoose ARs (a) Prepare the notional journal entry, as at 1 April 2002 or at 31 March 2018, to eliminate the Parent Ltd asset 'Investment in Subsidiary Ltd' and to eliminate the parent's portion of equity in the Subsidiary Ltd, in accordance with NZ IFRS 10 Consolidated Financial Statements and NZ IFRS3 Business Combinations Note: Your workings must be included on each line of your notional journal entry (b) Prepare the notional journal entry at 1 April 2002 to identify the non-controlling interest NZ IFRS 10 Consolidated Financial Statements and NZ IFRS 3 Business Combinations. The (NCI), in Subsidiary Ltd, to be reported in the group accounts in accordance with directors of Parent Ltd require the NCI in Subsidiary Ltd to be measured at fair value, Note: Your workings must be included on each line of your notional journal entry. G (e) Prepare a 100 acquisition analysis to 'prove' your goodwill answers in (a) and (b) Part B Parent Lid acquired equity in Subsidiary Ltd on i April 2007. At that date, the identifiable net assets were considered to be fairly valued and the equity of Subsidiary Lid comprised: EN-F Share capital $370 000 160 000 25 000 S 555 000 Retained earnings Asset revaluation surplus Parent Ltd has requested your help in the preparation of their consolidated financial statements for the financial year ended 31 March 2018 and has provided you with the following information

Answer & Explanation

Solved by verified expert

Get Answers to Unlimited Questions

Join us to gain access to millions of questions and expert answers. Enjoy exclusive benefits tailored just for you!

Membership Benefits:

Unlimited Question Access with detailed Answers

Zin AI - 3 Million Words

10 Dall-E 3 Images

20 Plot Generations

Conversation with Dialogue Memory

No Ads, Ever!

Access to Our Best AI Platform: Zin AI - Your personal assistant for all your inquiries!