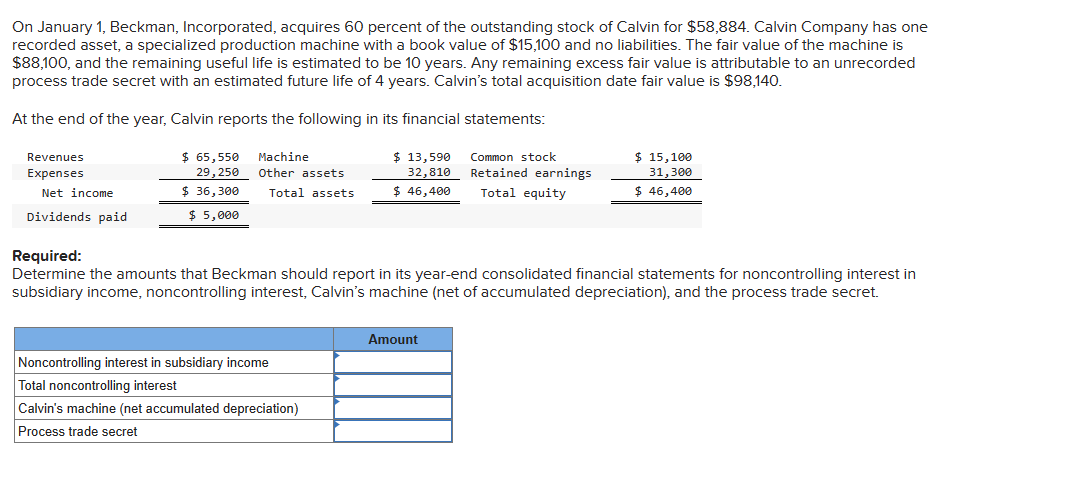

On January 1, Beckman, Incorporated, acquires 60 percent of the outstanding stock of Calvin for...

80.2K

Verified Solution

Question

Accounting

On January

On January

recorded asset, a specialized production machine with a book value of $

$

process trade secret with an estimated future life of

At the end of the year, Calvin reports the following in its financial statements:

Required:

Determine the amounts that Beckman should report in its year

subsidiary income, noncontrolling interest, Calvin's machine

Get Answers to Unlimited Questions

Join us to gain access to millions of questions and expert answers. Enjoy exclusive benefits tailored just for you!

Membership Benefits:

- Unlimited Question Access with detailed Answers

- Zin AI - 3 Million Words

- 10 Dall-E 3 Images

- 20 Plot Generations

- Conversation with Dialogue Memory

- No Ads, Ever!

- Access to Our Best AI Platform: Flex AI - Your personal assistant for all your inquiries!

Other questions asked by students

StudyZin's Question Purchase

1 Answer

$0.99

(Save $1 )

One time Pay

- No Ads

- Answer to 1 Question

- Get free Zin AI - 50 Thousand Words per Month

Best

Unlimited

$4.99*

(Save $5 )

Billed Monthly

- No Ads

- Answers to Unlimited Questions

- Get free Zin AI - 3 Million Words per Month

*First month only

Free

$0

- Get this answer for free!

- Sign up now to unlock the answer instantly

You can see the logs in the Dashboard.