Items 1 through 5 present various independent factual situations an auditor might encounter in conducting...

60.1K

Verified Solution

Link Copied!

Question

Accounting

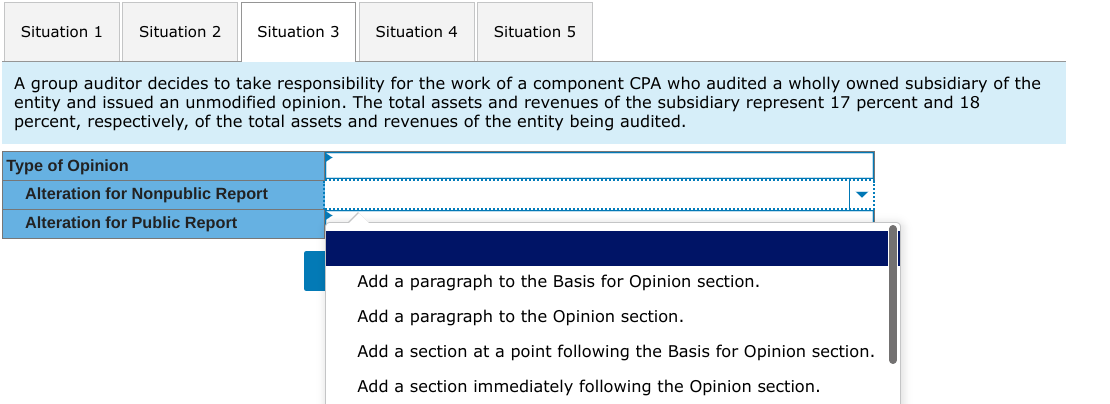

Items 1 through 5 present various independent factual situations an auditor might encounter in conducting an audit of a nonpublic company. For each situation, assume: - The auditor is independent. - The auditor previously expressed an unmodified opinion on the prior year's financial statements. - The nonpublic audit client is presenting single-year (not comparative) financial statements. - The conditions for an unmodified opinion exist unless contradicted in the factual situations. - The conditions stated in the factual situations are material. - No report modifications are to be made except in response to the factual situation. - The Report Alteration part of the problem only addresses the need to add an additional section or a paragraph to an existing section. Other parts of the audit report may be affected that are not examined in this question. Required: Below are the types of opinions the auditor ordinarily would issue and report modifications (if any) relating to an additional paragraph or section that would be necessary. Select as the best answer for each situation (items 1 through 5) the type of opinion and alterations, if any, the auditor would normally select. For each situation (items 1 through 5) also provide the report alteration under PCAOB standards for audits of public companies. A group auditor decides to take responsibility for the work of a component CPA who audited a wholly owned subsidiary of the entity and issued an unmodified opinion. The total assets and revenues of the subsidiary represent 17 percent and 18 percent, respectively, of the total assets and revenues of the entity being audited. A group auditor decides to take responsibility for the work of a component CPA who audited a wholly owned subsidiary of the entity and issued an unmodified opinion. The total assets and revenues of the subsidiary represent 17 percent and 18 percent, respectively, of the total assets and revenues of the entity being audited. A group auditor decides to take responsibility for the work of a component CPA who audited a wholly owned subsidiary of the entity and issued an unmodified opinion. The total assets and revenues of the subsidiary represent 17 percent and 18 percent, respectively, of the total assets and revenues of the entity being audited. A group auditor decides to take responsibility for the work of a component CPA who audited a wholly owned subsidiary of the entity and issued an unmodified opinion. The total assets and revenues of the subsidiary represent 17 percent and 18 percent, respectively, of the total assets and revenues of the entity being audited. A group auditor decides to take responsibility for the work of a component CPA who audited a wholly owned subsidiary of the entity and issued an unmodified opinion. The total assets and revenues of the subsidiary represent 17 percent and 18 percent, respectively, of the total assets and revenues of the entity being audited. A group auditor decides to take responsibility for the work of a component CPA who audited a wholly owned subsidiary of the entity and issued an unmodified opinion. The total assets and revenues of the subsidiary represent 17 percent and 18 percent, respectively, of the total assets and revenues of the entity being audited. Items 1 through 5 present various independent factual situations an auditor might encounter in conducting an audit of a nonpublic company. For each situation, assume: - The auditor is independent. - The auditor previously expressed an unmodified opinion on the prior year's financial statements. - The nonpublic audit client is presenting single-year (not comparative) financial statements. - The conditions for an unmodified opinion exist unless contradicted in the factual situations. - The conditions stated in the factual situations are material. - No report modifications are to be made except in response to the factual situation. - The Report Alteration part of the problem only addresses the need to add an additional section or a paragraph to an existing section. Other parts of the audit report may be affected that are not examined in this question. Required: Below are the types of opinions the auditor ordinarily would issue and report modifications (if any) relating to an additional paragraph or section that would be necessary. Select as the best answer for each situation (items 1 through 5) the type of opinion and alterations, if any, the auditor would normally select. For each situation (items 1 through 5) also provide the report alteration under PCAOB standards for audits of public companies. A group auditor decides to take responsibility for the work of a component CPA who audited a wholly owned subsidiary of the entity and issued an unmodified opinion. The total assets and revenues of the subsidiary represent 17 percent and 18 percent, respectively, of the total assets and revenues of the entity being audited. A group auditor decides to take responsibility for the work of a component CPA who audited a wholly owned subsidiary of the entity and issued an unmodified opinion. The total assets and revenues of the subsidiary represent 17 percent and 18 percent, respectively, of the total assets and revenues of the entity being audited. A group auditor decides to take responsibility for the work of a component CPA who audited a wholly owned subsidiary of the entity and issued an unmodified opinion. The total assets and revenues of the subsidiary represent 17 percent and 18 percent, respectively, of the total assets and revenues of the entity being audited. A group auditor decides to take responsibility for the work of a component CPA who audited a wholly owned subsidiary of the entity and issued an unmodified opinion. The total assets and revenues of the subsidiary represent 17 percent and 18 percent, respectively, of the total assets and revenues of the entity being audited. A group auditor decides to take responsibility for the work of a component CPA who audited a wholly owned subsidiary of the entity and issued an unmodified opinion. The total assets and revenues of the subsidiary represent 17 percent and 18 percent, respectively, of the total assets and revenues of the entity being audited. A group auditor decides to take responsibility for the work of a component CPA who audited a wholly owned subsidiary of the entity and issued an unmodified opinion. The total assets and revenues of the subsidiary represent 17 percent and 18 percent, respectively, of the total assets and revenues of the entity being audited

Answer & Explanation

Solved by verified expert

Get Answers to Unlimited Questions

Join us to gain access to millions of questions and expert answers. Enjoy exclusive benefits tailored just for you!

Membership Benefits:

Unlimited Question Access with detailed Answers

Zin AI - 3 Million Words

10 Dall-E 3 Images

20 Plot Generations

Conversation with Dialogue Memory

No Ads, Ever!

Access to Our Best AI Platform: Zin AI - Your personal assistant for all your inquiries!