70.2K

Verified Solution

Link Copied!

Link Copied!

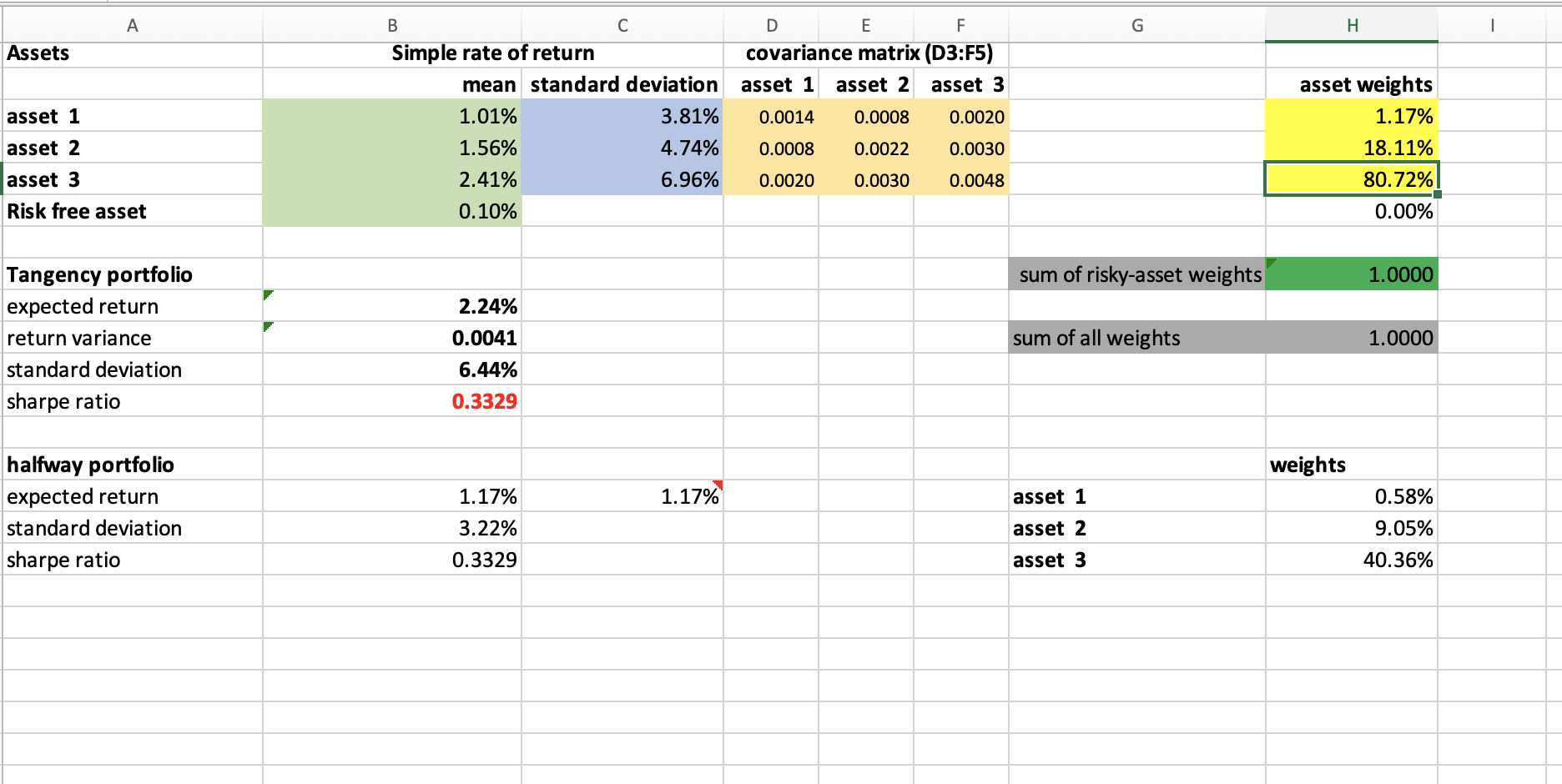

How to Calculate the asset weights with these data?

A G H I Assets B Simple rate of return mean standard deviation 1.01% 3.81% 1.56% 4.74% 2.41% 6.96% 0.10% D E F covariance matrix (D3:F5) asset 1 asset 2 asset 3 0.0014 0.0008 0.0020 asset 1 asset 2 0.0008 0.0022 0.0030 asset weights 1.17% 18.11% 80.72% 0.00% 0.0020 0.0030 0.0048 asset 3 Risk free asset sum of risky-asset weights 1.0000 2.24% Tangency portfolio expected return return variance standard deviation sharpe ratio 0.0041 sum of all weights 1.0000 6.44% 0.3329 weights 1.17% halfway portfolio expected return standard deviation sharpe ratio 1.17% 3.22% asset 1 asset 2 0.58% 9.05% 40.36% 0.3329 asset 3 A G H I Assets B Simple rate of return mean standard deviation 1.01% 3.81% 1.56% 4.74% 2.41% 6.96% 0.10% D E F covariance matrix (D3:F5) asset 1 asset 2 asset 3 0.0014 0.0008 0.0020 asset 1 asset 2 0.0008 0.0022 0.0030 asset weights 1.17% 18.11% 80.72% 0.00% 0.0020 0.0030 0.0048 asset 3 Risk free asset sum of risky-asset weights 1.0000 2.24% Tangency portfolio expected return return variance standard deviation sharpe ratio 0.0041 sum of all weights 1.0000 6.44% 0.3329 weights 1.17% halfway portfolio expected return standard deviation sharpe ratio 1.17% 3.22% asset 1 asset 2 0.58% 9.05% 40.36% 0.3329 asset 3

Answer & Explanation

Solved by verified expert