cost accounting BREEDEN SECURITY, INC. (B) In October 2007, as Marlene...

60.1K

Verified Solution

Link Copied!

Question

Accounting

cost accounting

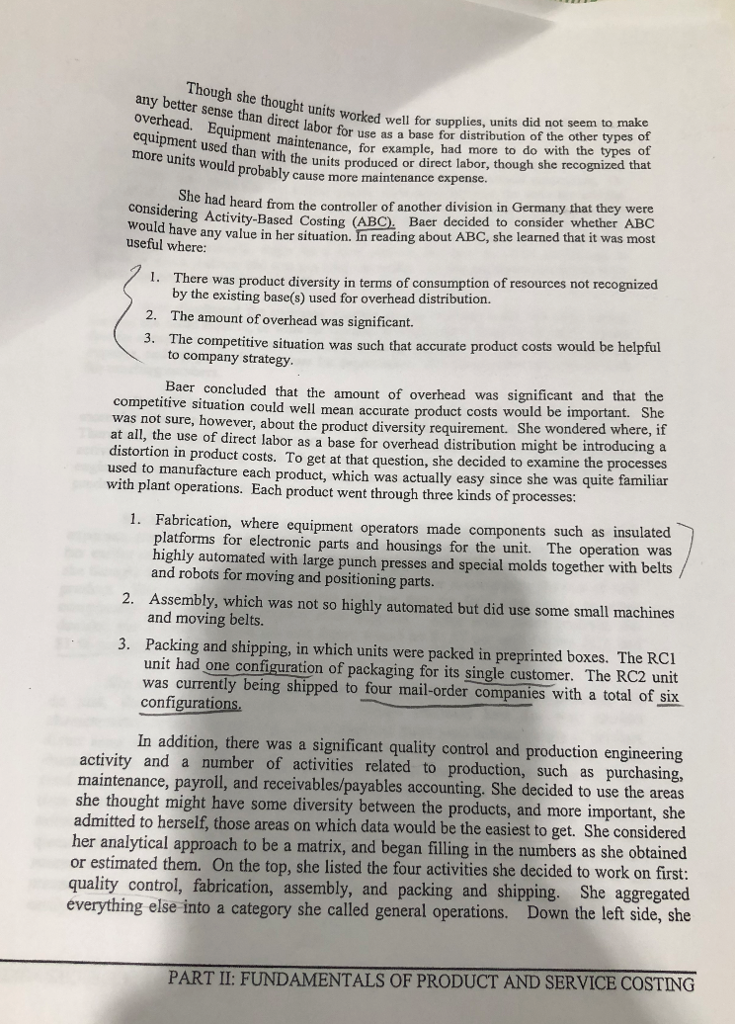

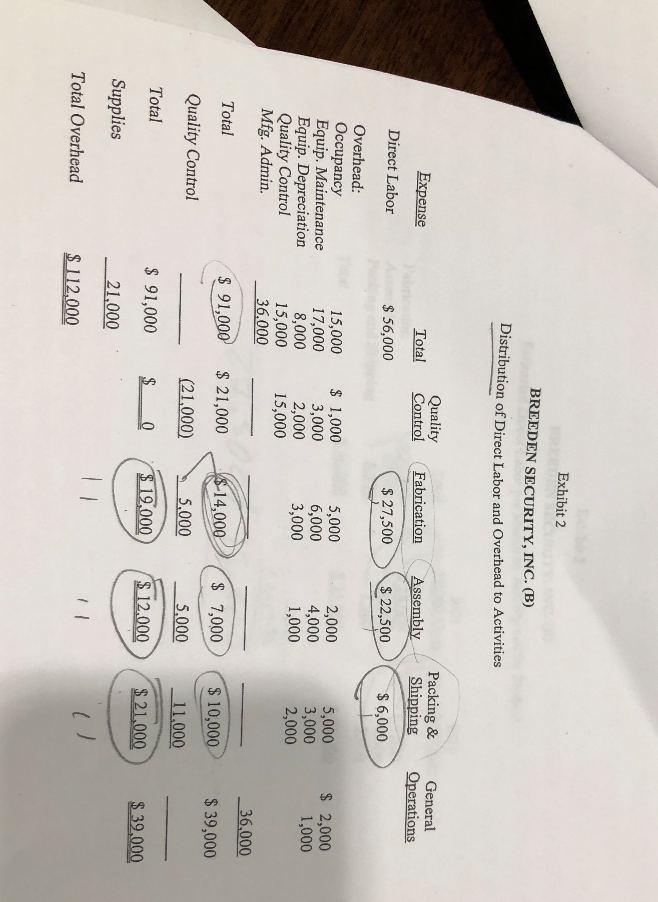

BREEDEN SECURITY, INC. (B) In October 2007, as Marlene Baer, Controller of Breeden Security USA, was wng te budget for Breeden's 2008 operations (Exhibit 1), she began to wonder about some of the assumptions built into her calculations. For example, she had used direct labor as a base for distributing indirect manufacturing overhead because that was the system traditionally used by the parent company. She recognized that the assumption on which that system was based was that the amount of direct labor used by a product was a good predictor of the proportion of manufacturing capacity used and thus a good indicator of the amount of overhead that should be charged to it. THE COMPANY In early 2007, Breeden Security GmbH, a large German manufacturer of radio equipment, had set up a subsidiary in the United States to manufacture two products Breeden had successfully marketed in Europe. One was a miniature signaling device used primarily for remote operation of garage doors. These "RCI" units consisted ofa signal sender, about half the size of a pack of cards, and a receiver, which was a bit larger. They contained a high-security chip which gave them an advantage over almost all the other units in the marketplace. A large manufacturer of motorized garage doors had agreed to take a minimum of 100,000 RI control units a year. Klein (the division president) and Baer thought that 120,000 units was a reasonable target for 2008 from this customer. Breeden also had designed a similar device that could be used by a householder to turn on inside lights when arriving after dark. This unit, called "RC2," was slightly more expensive to make since the receiving part was a complete plug-in device, while the RCI receiver was a component of the garage door unit. Initially, Breeden expected to sell the RC2 unit primarily through mail-order catalogues. Klein and Baer projected sales of 60,000 of these units for 2008. USING ABC TO ALLOCATE OVERHEAD Upon reflection, Baer didn't think that direct labor was predictor of the amount of overhead that should be charged to a product. She wondered whether units might be a better predictor, and decided that units worked well only as a predictor of supplies usage. Supplies consisted of wire, connectors, solder, some general types of resistors, and other parts and pieces. To measure how each product actually consumed supplies would be tedious, but she thought a reasonable estimate could be made. She would deal with that later. CASE: BREEDEN SECURITY, INC. (B) 45 BREEDEN SECURITY, INC. (B) In October 2007, as Marlene Baer, Controller of Breeden Security USA, was wng te budget for Breeden's 2008 operations (Exhibit 1), she began to wonder about some of the assumptions built into her calculations. For example, she had used direct labor as a base for distributing indirect manufacturing overhead because that was the system traditionally used by the parent company. She recognized that the assumption on which that system was based was that the amount of direct labor used by a product was a good predictor of the proportion of manufacturing capacity used and thus a good indicator of the amount of overhead that should be charged to it. THE COMPANY In early 2007, Breeden Security GmbH, a large German manufacturer of radio equipment, had set up a subsidiary in the United States to manufacture two products Breeden had successfully marketed in Europe. One was a miniature signaling device used primarily for remote operation of garage doors. These "RCI" units consisted ofa signal sender, about half the size of a pack of cards, and a receiver, which was a bit larger. They contained a high-security chip which gave them an advantage over almost all the other units in the marketplace. A large manufacturer of motorized garage doors had agreed to take a minimum of 100,000 RI control units a year. Klein (the division president) and Baer thought that 120,000 units was a reasonable target for 2008 from this customer. Breeden also had designed a similar device that could be used by a householder to turn on inside lights when arriving after dark. This unit, called "RC2," was slightly more expensive to make since the receiving part was a complete plug-in device, while the RCI receiver was a component of the garage door unit. Initially, Breeden expected to sell the RC2 unit primarily through mail-order catalogues. Klein and Baer projected sales of 60,000 of these units for 2008. USING ABC TO ALLOCATE OVERHEAD Upon reflection, Baer didn't think that direct labor was predictor of the amount of overhead that should be charged to a product. She wondered whether units might be a better predictor, and decided that units worked well only as a predictor of supplies usage. Supplies consisted of wire, connectors, solder, some general types of resistors, and other parts and pieces. To measure how each product actually consumed supplies would be tedious, but she thought a reasonable estimate could be made. She would deal with that later. CASE: BREEDEN SECURITY, INC. (B) 45

Answer & Explanation

Solved by verified expert

Get Answers to Unlimited Questions

Join us to gain access to millions of questions and expert answers. Enjoy exclusive benefits tailored just for you!

Membership Benefits:

Unlimited Question Access with detailed Answers

Zin AI - 3 Million Words

10 Dall-E 3 Images

20 Plot Generations

Conversation with Dialogue Memory

No Ads, Ever!

Access to Our Best AI Platform: Zin AI - Your personal assistant for all your inquiries!