Case 5.3Fly-by-Night International Group: Can This Company Be Saved? Douglas C. Mather, founder, chair, and...

60.1K

Verified Solution

Question

Accounting

Case 5.3Fly-by-Night International Group: Can This Company Be Saved?

Douglas C. Mather, founder, chair, and chief executive ofFly-by-Night International Group (FBN), lived the fast-paced, risk-seeking life that he tried to inject into his company. Flying the company's Learjets, he logged 28 world speed records. Once he throttled a company plane to the top of Mount Everest in three-and-a-half-minutes.

These activities seemed perfectly appropriate at the time. Mather was a Navy fighter pilot in Vietnam and then flew commercial airlines. In the mid-1970s, he started FBN as a pilot training school. With the defense buildup beginning in the early 1980s, Mather branched out into government contracting. He equipped the company's Learjets with radar jammers and other sophisticated electronic devices to mimic enemy aircraft. He then contracted his "rent-an-enemy" fleet to the Navy and Air Force for use in fighter pilot training. The Pentagon liked the idea, and FBN's revenues grew to $55 million in the fiscal year ending April 30, Year 14. Its common stock, issued to the public in Year 9 at $8.50 a share, reached a high of $16.50 in mid-Year 13. Mather and FBN received glowing write-ups inBusiness WeekandFortune.

In mid-Year 14, however, FBN began a rapid descent. Although still growing rapidly, its cash flow was inadequate to service its debt. According to Mather, he was "just dumbfounded. There was never an inkling of a problem with cash."

In the fall of Year 14, the board of directors withdrew the company's financial statements for the year ending April 30, Year 14, stating that there appeared to be material misstatements that needed investigation. In December of Year 14, Mather was asked to step aside as manager and director of the company pending completion of an investigation of certain transactions between Mather and the company. On December 29, Year 14, NASDAQ (over-the-counter stock market) discontinued quoting the company's common shares. In February, Year 15, following its investigation, the board of directors terminated Mather's employment and membership on the board.

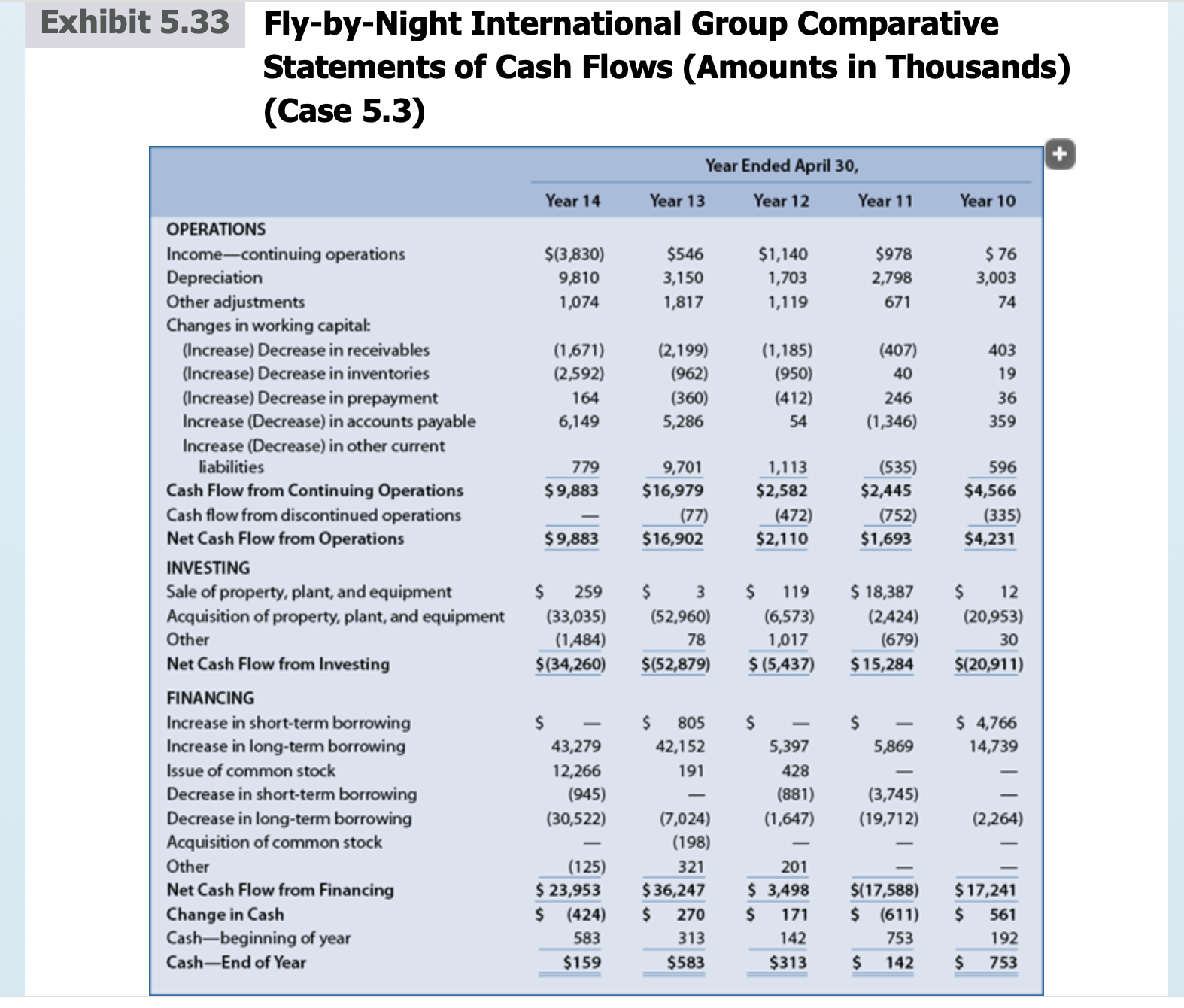

Exhibits 5.31,5.32, and5.33present the financial statements and related notes of FBN for the five years ending April, Year 10, through April, Year 14. The financial statements for Year 10 to Year 12 use the amounts originally reported for each year. The amounts reported on the statement of cash flows for Year 10 (for example, the change in accounts receivable) do not precisely reconcile to the amounts on the balance sheet at the beginning and end of the year because certain items classified as relating tocontinuing operations on the balance sheet at the end of Year 9 were reclassified as relating to discontinued operations on the balance sheet at the end of Year 10. The financial statements for Year 13 and Year 14 represent the restated financial statements for those years after the board of directors completed its investigation of suspected material misstatements that caused it to withdraw the originally issued financial statements for fiscal Year 14.Exhibit 5.34lists the members of the board of directors.Exhibit 5.35presents profitability and risk ratios for FBN.

Required

Case Study the following questions

- What evidence do you observe from analyzing the financial statements that might signal the cash flow problems experienced in mid-Year 14?

- Can FBN avoid bankruptcy during Year 15? What changes in the design or implementation of FBN's strategy would you recommend? To compute Altman's Z-score, use the low-bid market price for the year to determine the market value of common shareholders' equity.

Notes to Financial Statements1. Summary of Significant Accounting Policies

Consolidation.The consolidated financial statements include the accounts of the company and its wholly owned subsidiaries. The company uses the equity method for subsidiaries that are not majority owned (50% or less) and eliminates significant intercompany transactions and balances.

Inventories.Inventories, which consist of aircraft fuel, spare parts, and supplies, appear at lower of FIFO cost or market.

Property and Equipment.Property and equipment appear at acquisition cost. The company capitalizes major inspections, renewals, and improvements, while it expenses replacements, maintenance, and repairs that do not improve or extend the life of the respective assets. The company computes depreciation of property and equipment using the straight-line method.

Contract Income Recognition.Contractual specifications (such as revenue rates, reimbursement terms, and functional considerations) vary among contracts; accordingly, the company recognizes guaranteed contract income (guaranteed revenue minus related direct costs) as it logs flight hours or on a straight-line monthly basis over the contract year, whichever method better reflects the economics of the contract. The company recognizes income from discretionary hours flown in excess of the minimum guaranteed amount each month as it logs such discretionary hours.

Income Taxes.The company recognizes deferred income taxes for temporary differences between financial and tax reporting amounts.

2. Transactions with Major Customers

The company provides contract flight services to three major customers: the U.S. Air Force, the U.S. Navy, and the Federal Reserve Bank System. These contracts have termination dates in Year 16 or Year 17. Revenues from all government contracts as a percentage of total revenues were as follows: Year 14, 62%; Year 13, 72%; Year 12, 73%; Year 11, 68%; and Year 10, 31%.

3. Segment Data

During Year 10, the company operated in the following five business segments:

Flight OperationsBusiness.Provides combat readiness training to the military and nightly transfer of negotiable instruments for the Federal Reserve Bank System, both under multiyear contracts.

Flight OperationsTransport.Provides charter transport services to a variety of customers.

Fixed-Base Operations.Provides ground support operations (fuel and maintenance) to commercial airlines at several major airports.

Education and Training.Provides training for nonmilitary pilots.

Aircraft Sales and Leasing.Acquires aircraft that the company then resells or leases to various firms.

The company discontinued the Flight OperationsTransport and Education and Training segments in Year 11. It sold most of the assets of the Aircraft Sales and Leasing segment in Year 11.

Segment revenue, operating profit, and asset data for the various segments are as follows (amounts in thousands):

aIncludes a gain of $1.2 million on the sale of aircraft.

bIncludes a gain of $2.6 million on the sale of aircraft.

4. Discontinued Operations

Income from discontinued operations consists of the following (amounts in thousands):

5. Related-Party Transactions

On April 30, Year 11, the company sold most of the net assets of the Aircraft Sales and Leasing segment to Interlease, Inc., a Georgia corporation wholly owned by the company's majority stockholder, whose personal holdings at that time represented approximately 75% of the company.

Under the terms of the sale, the sales price was $1,368,000, of which the buyer paid $368,000 in cash and gave a promissory note for the remaining $1,000,000. The company treated the proceeds received in excess of the book value of the net assets sold of $712,367 as a capital contribution due to the related-party nature of the transaction. FBN originally acquired the assets of the Aircraft Sales and Leasing segment during Year 10.

On September 29, Year 14, FBN's board of directors established a Transaction Committee to examine certain transactions between the company and Douglas Mather, FBN's chair, president, and majority stockholder. These transactions appear here.

Certain Loans to Mather.In early September, Year 13, the board of directors authorized a $1 million loan to Mather at the company's cost of borrowing plus. On September 19, Year 13, Mather tendered a $1 million check to the company in repayment of the loan. On September 22, Year 13, at Mather's direction, the company made an additional $1 million loan to him, the proceeds of which Mather apparently used to cover his check in repayment of the first $1 million loan. The Transaction Committee concluded that the board of directors did not authorize the September 22, Year 13, loan to Mather, nor was any director other than Mather aware of the loan at the time. The company's Year 13 Proxy Statement, dated September 27, Year 13, incorrectly stated that "as of September 19, Year 13, Mather had repaid the principal amount of his indebtedness to the company." Mather's $1 million loan remained outstanding until it was canceled in connection with the ESOP (employee stock ownership plan) transaction discussed next.

ESOP Transaction.On February 28, Year 14, the company's ESOP acquired 100,000 shares of the company's common stock from Mather at $14.25 per share. FBN financed the purchase. The ESOP gave the company a $1,425,000 unsecured demand note. To complete the transaction, the company canceled a $1,000,000 promissory note from Mather and paid the remaining $425,000 in cash. The Transaction Committee determined that the board of directors did not authorize the $1,425,000 loan to the ESOP, the cancellation of Mather's $1,000,000 note, or the payment of $425,000 in cash.

Eastwind Transaction.On April 27, Year 14, the company acquired four Eastwind aircraft from a German company. FBN subsequently sold these aircraft to Transreco, a corporation owned by Douglas Mather, for a profit of $1,600,000. In late September and early October, Transreco sold these four aircraft at a profit of $780,000 to unaffiliated third parties. The Transactions Committee determined that none of the officers or directors of the company were aware of the Eastwind transaction until late September, Year 14.

On December 12, Year 14, the company announced that Mather had agreed to step aside as chair and director and take no part in management of the company pending resolution of the matters presented to the board by the Transactions Committee. On February 13, Year 15, the company announced that it had entered into a settlement agreement with Mather and Transreco resolving certain of the issues addressed by the Transactions Committee. Pursuant to the agreement, the company will receive $211,000, the bonus paid to Mather for fiscal Year 14, and $780,000, the gain recognized by Transreco on the sale of the Eastwind aircraft. Also pursuant to the settlement, Mather will resign all positions with the company and waive his rights under his employment agreement to any future compensation or benefits to which he might otherwise have a claim.

6. Long-Term Debt

Long-term debt consists of the following (amounts in thousands):

Substantially all of the company's property, plant, and equipment serve as collateral for this debt. The borrowings from bank and finance companies contain restrictive covenants, the most restrictive of which appear in the following table:

| Year 14 | Year 13 | Year 12 | Year 11 | Year 10 | |

|---|---|---|---|---|---|

| Liabilities/Tangible net worth | |||||

| Tangible net worth | >$20,000 | >$5,800 | >$5,400 | >$5.300 | >$5,100 |

| Working capital | >$5,000 | ||||

| Interest coverage ratio | >1.15 |

As of April 30, Year 14, the company is in default of its debt covenants. It is also in default with respect to covenants underlying its capitalized lease obligations. As a result, lenders have the right to accelerate repayment of their loans. Accordingly, the company has classified all of its long-term debt as a current liability.

The company has entered into operating leases for aircraft and other equipment. The estimated present value of the minimum lease payments under these operating leases as of April 30 of each year is as follows:

| Year 14 | $2,706 |

| Year 13 | 3,142 |

| Year 12 | 3,594 |

| Year 11 | 3,971 |

| Year 10 | 4,083 |

7. Income Taxes

Income tax expense consists of the following:

The cumulative tax loss and tax credit carryovers as of April 30 of each year are as follows:

| April 30, | Tax Loss | Tax Credit |

|---|---|---|

| Year 14 | $10,300 | $250 |

| Year 13 | 5,200 | 280 |

| Year 12 | 1,400 | 300 |

| Year 11 | 2,100 | 450 |

| Year 10 | 4,500 | 750 |

The deferred tax provision results from temporary differences in the recognition of revenues and expenses for income tax and financial reporting. The sources and amounts of these differences for each year are as follows:

A reconciliation of the effective tax rate with the statutory tax rate is as follows:

8. Market Price Information

The company's common stock trades on the NASDAQ National Market System under the symbol FBN. Trading in the company common stock commenced on January 10, Year 10. High- and low-bid prices during each fiscal year are as follows:

| Fiscal Year | High Bid | Low Bid |

|---|---|---|

| Year 14 | $16.50 | $9.50 |

| Year 13 | 14.63 | 6.25 |

| Year 12 | 11.25 | 3.25 |

| Year 11 | 4.63 | 3.00 |

| Year 10 | 5.25 | 3.25 |

On December 29, Year 14, the company announced that NASDAQ had decided to discontinue quoting the company's common stock because of the company's failure to comply with NASDAQ's filing requirements.

Ownership of the company's stock at various dates appears as follows:

Get Answers to Unlimited Questions

Join us to gain access to millions of questions and expert answers. Enjoy exclusive benefits tailored just for you!

Membership Benefits:

- Unlimited Question Access with detailed Answers

- Zin AI - 3 Million Words

- 10 Dall-E 3 Images

- 20 Plot Generations

- Conversation with Dialogue Memory

- No Ads, Ever!

- Access to Our Best AI Platform: Zin AI - Your personal assistant for all your inquiries!

Other questions asked by students

The population P(t) of a culture of the bacterium Pseudomonas aeruginosa is given by P(t)=-1687t2...

StudyZin's Question Purchase

1 Answer

$0.99

(Save $1 )

One time Pay

- No Ads

- Answer to 1 Question

- Get free Zin AI - 50 Thousand Words per Month

Unlimited

$4.99*

(Save $5 )

Billed Monthly

- No Ads

- Answers to Unlimited Questions

- Get free Zin AI - 3 Million Words per Month

*First month only

Free

$0

- Get this answer for free!

- Sign up now to unlock the answer instantly

You can see the logs in the Dashboard.