Assume: Spot Date April 26, 2021 Three and ten year bond futures expiry September...

50.1K

Verified Solution

Link Copied!

Question

Finance

Assume:

Spot Date April 26, 2021

Three and ten year bond futures expiry September 15, 2021

You sell 125 three year bond futures contracts at 99.67and buy 41 ten year contracts at 98.31. You hold your position for 3 days then close everything out. What would the variation margin be on each day(for each position and aggregated) if the following were the prices over your holding period. What is the total profit or loss once the positions are closed out:

Assume that initial margin is 5%.

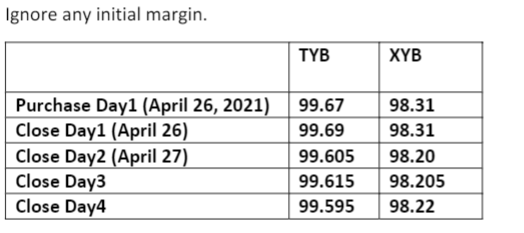

Ignore any initial margin. TYB XYB Purchase Day1 (April 26, 2021) Close Day1 (April 26) Close Day2 (April 27) Close Day3 Close Day4 99.67 99.69 99.605 99.615 99.595 98.31 98.31 98.20 98.205 98.22

Answer & Explanation

Solved by verified expert

Get Answers to Unlimited Questions

Join us to gain access to millions of questions and expert answers. Enjoy exclusive benefits tailored just for you!

Membership Benefits:

Unlimited Question Access with detailed Answers

Zin AI - 3 Million Words

10 Dall-E 3 Images

20 Plot Generations

Conversation with Dialogue Memory

No Ads, Ever!

Access to Our Best AI Platform: Zin AI - Your personal assistant for all your inquiries!