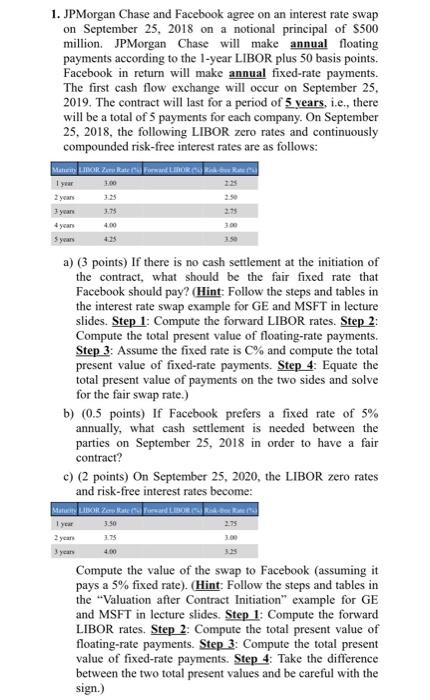

1. JPMorgan Chase and Facebook agree on an interest rate swap on September 25, 2018...

60.1K

Verified Solution

Link Copied!

Question

Finance

1. JPMorgan Chase and Facebook agree on an interest rate swap on September 25, 2018 on a notional principal of $500 million. JPMorgan Chase will make annual floating payments according to the 1-year LIBOR plus 50 basis points. Facebook in return will make annual fixed-rate payments. The first cash flow exchange will occur on September 25, 2019. The contract will last for a period of 5 years, i.e., there will be a total of 5 payments for each company. On September 25, 2018, the following LIBOR zero rates and continuously compounded risk-free interest rates are as follows: Matunity LOR.Zemes and LORER 1.00 1 year 2 years 3 years 3.75 275 4.00 405 5 years 150 a) (3 points) If there is no cash settlement at the initiation of the contract, what should be the fair fixed rate that Facebook should pay? (Hint: Follow the steps and tables in the interest rate swap example for GE and MSFT in lecture slides. Step 1: Compute the forward LIBOR rates. Step 2: Compute the total present value of floating-rate payments. Step 3: Assume the fixed rate is % and compute the total present value of fixed-rate payments. Step 4. Equate the total present value of payments on the two sides and solve for the fair swap rate.) b) (0.5 points) If Facebook prefers a fixed rate of 5% annually, what cash settlement is needed between the parties on September 25, 2018 in order to have a fair contract? c) (2 points) On September 25, 2020, the LIBOR zero rates and risk-free interest rates become: Miten LUDOR Zavate Board LIBORIS Bea 3.50 275 4.00 years 5. Compute the value of the swap to Facebook (assuming it pays a 5% fixed rate). (Hint: Follow the steps and tables in the "Valuation after Contract Initiation" example for GE and MSFT in lecture slides. Step 1: Compute the forward LIBOR rates. Step 2: Compute the total present value of floating-rate payments. Step 3: Compute the total present value of fixed-rate payments. Step 4: Take the difference between the two total present values and be careful with the sign.) 1. JPMorgan Chase and Facebook agree on an interest rate swap on September 25, 2018 on a notional principal of $500 million. JPMorgan Chase will make annual floating payments according to the 1-year LIBOR plus 50 basis points. Facebook in return will make annual fixed-rate payments. The first cash flow exchange will occur on September 25, 2019. The contract will last for a period of 5 years, i.e., there will be a total of 5 payments for each company. On September 25, 2018, the following LIBOR zero rates and continuously compounded risk-free interest rates are as follows: Matunity LOR.Zemes and LORER 1.00 1 year 2 years 3 years 3.75 275 4.00 405 5 years 150 a) (3 points) If there is no cash settlement at the initiation of the contract, what should be the fair fixed rate that Facebook should pay? (Hint: Follow the steps and tables in the interest rate swap example for GE and MSFT in lecture slides. Step 1: Compute the forward LIBOR rates. Step 2: Compute the total present value of floating-rate payments. Step 3: Assume the fixed rate is % and compute the total present value of fixed-rate payments. Step 4. Equate the total present value of payments on the two sides and solve for the fair swap rate.) b) (0.5 points) If Facebook prefers a fixed rate of 5% annually, what cash settlement is needed between the parties on September 25, 2018 in order to have a fair contract? c) (2 points) On September 25, 2020, the LIBOR zero rates and risk-free interest rates become: Miten LUDOR Zavate Board LIBORIS Bea 3.50 275 4.00 years 5. Compute the value of the swap to Facebook (assuming it pays a 5% fixed rate). (Hint: Follow the steps and tables in the "Valuation after Contract Initiation" example for GE and MSFT in lecture slides. Step 1: Compute the forward LIBOR rates. Step 2: Compute the total present value of floating-rate payments. Step 3: Compute the total present value of fixed-rate payments. Step 4: Take the difference between the two total present values and be careful with the sign.)

Answer & Explanation

Solved by verified expert

Get Answers to Unlimited Questions

Join us to gain access to millions of questions and expert answers. Enjoy exclusive benefits tailored just for you!

Membership Benefits:

Unlimited Question Access with detailed Answers

Zin AI - 3 Million Words

10 Dall-E 3 Images

20 Plot Generations

Conversation with Dialogue Memory

No Ads, Ever!

Access to Our Best AI Platform: Zin AI - Your personal assistant for all your inquiries!